Almost a decade ago, Carnegie Mellon professors Sarah Laschever and Linda Babcock found that men ask for raises and promotions four times more than women do. Their research has now been cited so often that it’s just about become popular wisdom.

But a new study by researchers at London’s Cass Business School, the University of Warwick, and the University of Wisconsin analyzed a random sample of just over 4,500 workers across 800 employers in Australia and found something surprising: Women aren’t afraid of asking for raises and promotions. Women ask as often as their male counterparts, but they get what they want less often—25% less often, in fact.

NEW RESEARCH, NEW REACTIONS

Using a detailed series of questions, the researchers tackled two stubborn yet widespread beliefs surrounding the gender pay gap. The first—that women aren’t as ambitious or pushy as men—was found to have no basis in the study (which focused on Australia, because it’s the only country that gathers data on employees’ raise requests). The second—that women are more afraid of upsetting their bosses or hurting their relationships with their employers—was also thrown out.

These findings shift the burden from professional women to the companies that employ them. These days, it appears that closing the pay gap may be less about changing the ways women have been raised to understand the value of their work and more about how their employers react to women’s improving negotiating skills.

Social and political climates may have something to do with that shift. Earlier this year, the World Economic Forum (WEF) issued its annual report on the gender gap, and it didn’t just fall into the void. Just last month, in Iceland, where women earn an average of 14% less than men, women left their desks at 2:38 p.m., leaving their workdays 14% unfinished—right at the point where that pay discrepancy kicked in.

Taking to the streets and leaving desktops unwatched might not catch on in the U.S., but the metaphor is instructive. The WEF report looked at 144 countries and measured the gaps not only in economic opportunities but also in access to education, health care, and political representation. The U.S. ranked 45th on the list. At the current rate, researchers believe, women worldwide are not going to see these gaps close completely in their lifetimes—it will take 170 years at the current rates of progress worldwide.

Like this Article?Share It !You now can easily enjoy/follow/share Today our Award Winning Articles/Blogs with Now Over 2.5 Million Growing Participates Worldwidein our various Social Media formats below:

educate/collaborate/network….Look forward to your Participation !

Continue of article:

But as one of the coauthors of the Cass School study points out, that research “potentially has an upside. Young women today are negotiating their pay and conditions more successfully than older females,” says Amanda Goodall, “and perhaps that will continue as they become more senior.” Women aren’t just negotiating more aggressively than in the past. They’re now more aware that they aren’t being rewarded equitably for doing so.

Knowledge is power, in other words, and it spreads almost exponentially over time. It’s findings like Goodall’s and her fellow researchers’ that don’t just document a problem but empower those who are hurt by it to demand change in the right places.

WHAT WORKING WOMEN CAN DO STARTING NOW

With that in mind, there are a few steps women can take right away to begin pressing to earn what they’re worth.

Know your own value. Do the research and honestly assess your talents, skills, and experiences—because your boss won’t do this for you. Get the data on pay for the same or comparable jobs in your community, so you have objective (or at least less subjective) information with which to build a case for yourself.

I was so proud when a former intern of mine was offered a position at a major tech company and asked me what to do before accepting. She’d done her research, and the firm’s salary offer was toward the top for comparable positions. Still, she said, “I know I should negotiate something.” She was right; I advised her to think about non-salary compensation that she’d value, and she ended up getting her new employer to pay for her move.

Be your own advocate. Investigate the culture of your company, how decisions are made, and what’s valued most (and least). It’s one thing to do the “hard” research—salary benchmarks and so on—and another to get a “softer,” qualitative feel for an employer’s mind-set around compensation. This holds true as much for a company you’re considering working for as one you already do work for.

Go on Glassbreakers to get or become a mentor, and LinkedIn to connect with others in your field. Read reviews on Fairygodboss. Talk to trusted coworkers. Reach out to past employees who’ve since moved on, and ask their experiences. Then use your research to help you speak up—not just about your salary offer or about that promotion coming up, but about ways in which women’s leadership can add value to their bottom line.

Outside of work, too, it’s important for professional women to understand policymakers’ priorities; change happens in both big and incremental ways. The keys to more opportunities and important social shifts can often be found in the details of all kinds of bills, from the municipal to the federal level.

Face the chaos with courage. When I left my first CEO position, a member of the board asked me what I thought was one of most important qualifications for the job. Courage was the answer that came out of my mouth before I had a chance to think. I still believe that courage is what it takes to act in the midst of chaos and against long odds that you shouldn’t have to surmount but are forced to. It takes courage, too, to own the responsibility for fixing something, even if you don’t have total authority to—and to make decisions even when you can’t guarantee the outcomes.

It’s possible to see the latest research as different fragments of the same picture. Women have changed—even in the past decade—but the world at large has not, and 170 years is too long to wait for parity. The U.S. has just fallen short of electing its first female president, but it’s worth remembering that Hillary Clinton won the popular vote. That means that a majority of American voters still wanted a woman to represent them, and that desire doesn’t vanish.

Whatever the next four years turn out to look like, it’s clear that the social tide is turning. Younger women are asking for their due when their older colleagues didn’t dare to (often as a result of wholly valid fears). It’s heartening to know that the data confirms what many of us have long hoped: Finally, women know their worth. Now it’s time for everyone else to catch up. Don’t worry—we’ll show you the way.

https://www.firstsun.com/wp-content/uploads/2016/07/free-women-at-meeting.jpeg350524First Sun Teamhttps://www.firstsun.com/wp-content/uploads/2018/05/logo-min-300x123.jpgFirst Sun Team2016-11-11 16:09:492020-09-30 20:50:11#Leadership : Actually, Women Do Ask For Raises As Often As Men—They Just Don’t Get Them…A Recent Study Shows that Women Know What they’re Worth and Aren’t Afraid to Ask for It. It’s Their Employers that Don’t.

Employee compensation can be an emotional subject, especially if you’re the employee. It is often daintily tiptoed around in interviews and loudly complained about in bars. Personally, I’m a firm believer that compensation is a reflection of an employee’s value to a company. As value goes up, so does pay.

When I express these opinions, however, I often get disgruntled rebuttals like, “Yeah, right. Corporations have no concept of loyalty”; “Layoffs are completely arbitrary—it doesn’t matter what you’re worth”; and, “The only way to get a raise is to change jobs!”

Since these complaints are made to me—the CEO of a company that clearly isn’t so callous—it’s obvious that these stereotypes cannot be universal. Putting aside this irony, though, even if every company in the world were as ruthless and coldblooded as some believe, value and compensation would still be inextricably connected. Let’s take a look at why this is the case and how you can increase your value as an employee to get paid what you deserve.

WHAT HAPPENS BEHIND CLOSED DOORS

Let’s be a fly on the wall in that dim, coffin-shaped room where lanky, black-suited business misers drum their spindly fingers together and cackle over that most evil of subjects: layoffs.

When they discuss the customer support floor, they decide they need to lay off one person, and gradually narrow the options down to two employees:

Option 1: “Bill” is an old-and-true company standby. He’s worked at the company for 20 years and has been completely faithful to his job expectations. He clocks in and out on time and delivers his customer support perfectly on script. As a result, he’s accumulated a number of raises over the years and now makes $20 an hour.

Option 2: “Shelly” has only worked in customer support for five years but has obtained advanced technical certifications, has an excellent interpersonal manner, and routinely turns upset customers into loyal patrons. Clients who get support from her are 30% more likely to purchase additional services and to refer friends.

She talks off script a fair amount but keeps track of what she says and how customers react. As a result, she has submitted many helpful modifications to the basic IT script, resulting in a 10% increase in customer satisfaction for the whole floor. Due to her high performance, Shelly also makes $20 per hour.

Which one gets the boot? It’s Bill without question.

The company is actually losing money on Bill. If they fired him, a new employee would work for only $12/hour and could read the script just as skillfully as Bill does within two weeks.

If Shelly were fired, however, the company would lose out on a major source of sales, referrals, customer satisfaction, and an internal system for improving the whole department—they can’t afford to lose her!

Like this Article?Share It !You now can easily enjoy/follow/share Today our Award Winning Articles/Blogs with Now Over 2.5 Million Growing Participates Worldwidein our various Social Media formats below:

educate/collaborate/network….Look forward to your Participation !

Continue of article:

VALUE IS NOT THE SAME THING AS YEARS ON THE JOB

But what about faithful old Bill? It would be so mean to fire him! Bill’s problem is that he hasn’t really done anything to justify his increased wages. Small raises have accumulated on his paycheck like moss on an old river rock, but his real value is still around $12 an hour.

However, since Bill has been working at the company for so many years, he probably “feels” like he’s worth $20 an hour. Never mind the fact that he couldn’t get paid $20 an hour at a different company, he’s “put in his time,” so he’s worth $20 an hour, right?

Now, I’m not trying to understate the value of experience and wisdom. Good employees learn and grow over time, so they provide more value for their employer. As a reward, they get raises. The problem is, those raises are often based on meeting minimum standards for specified periods of time—not the value an employee brings to the table. As a result, when push comes to shove and a company needs to actually evaluate the worth of an employee, “years on the job” means far less to the business than added value.

BUSINESSES PAY FOR VALUE, AND EMPLOYEES ARE THEIR ASSETS

Many employees are confused about what their salaries pay for. When people first enter the workforce as teenagers, they usually start with an hourly wage. The equation is simple: The more you work, the more money you get. Unfortunately, after a couple of years, many people begin to translate time into money and begin to think, “I’ve put in a lot of time at this job, so it stands to reason that I should be making a lot of money! I need a raise!”

Allow me to burst that bubble. Value isn’t a function of time. There are 24 hours in a day whether a company pays for them or not—it’s what you do with those hours that counts. Even for hourly employees, businesses aren’t paying for time—they’re paying for value. To put it simply, an employee is a company asset, and compensation is an investment in that asset.

Let me explain what I mean: If I were to invest $5,000 in a new asset for my business—say an online marketing account—you might think that I would have to make $5,000 in sales to justify the expense. Unfortunately, it doesn’t quite work that way. I won’t get too deep into the math of contribution margin, but in short, since my business expenses aren’t just limited to what I spend on marketing, it turns out that the account would have to make me at least three times my investment ($15,000) just to break even.

If the asset started producing four or five times more money than I put into it, then it would really be profitable. In fact, I’d be willing to invest more if I knew my payoff would be that good.

The same goes for employees: If I’m going to invest in people, I need to know that having them around will make my company at least three times what I’m paying them. The more revenue an employee drives for my business, the greater their value and the more I’m happy to pay to have them as an asset. An employee who produces less value, however, loses me money and—unless they can become more productive—I can’t afford to keep them in the long run.

Now, I think we’ve looked at things like a ruthless businessman for long enough to show why companies care about the value their employees bring to the table.

In most real businesses with real, warm-hearted people (like I try to be), the same principles are still at play, but the focus is more on encouraging employees to become more valuable than on eliminating dead weight. In general, this encouragement comes in the form of salary. The more value an employee brings to the table, the more they deserve to be paid. The question then becomes, how do employees increase their value?

There are three basic steps:

Ensure that you’re meeting the basic expectations of your job.

Identify areas where you can add more value.

Create and execute a plan to exceed expectations.

Step 1: Meet expectations. Before you start trying to expand your horizons, it’s a good idea to make sure that you’re at least fulfilling the minimum requirements of your role.

Of course, it can sometimes be hard to figure out what those requirements are. A recent Gallup poll revealed that up to half of employees don’t really understand what is expected of them at work. Many companies have very little in the way of formal job descriptions. Others have long lists of tasks and expectations around hiring time, but when you start the job you find that half the stuff on the list you never do and half the stuff you do isn’t on the list.

So if you’re not sure what your job expectations really are, the easiest way to get that question answered is to talk to your manager. Havea discussion about what workplace success looks like. You might even ask how your position adds value to the company. This gives you a target for increasing your value later on.

If, in this discussion, you discover work expectations that you weren’t aware of or that you haven’t been meeting, your first priority should be to start meeting those expectations. You may also find that, as Gallup’s poll also suggests, somemanagers are just as confused about your role as you are. If this describes your supervisors, then a sit-down conversation is especially important. Defining together what your core responsibilities are will help them to know when you are exceeding expectations.

[fusion_builder_container hundred_percent=”yes” overflow=”visible”][fusion_builder_row][fusion_builder_column type=”1_1″ background_position=”left top” background_color=”” border_size=”” border_color=”” border_style=”solid” spacing=”yes” background_image=”” background_repeat=”no-repeat” padding=”” margin_top=”0px” margin_bottom=”0px” class=”” id=”” animation_type=”” animation_speed=”0.3″ animation_direction=”left” hide_on_mobile=”no” center_content=”no” min_height=”none”][Related: 5 Ways To Get The Most Out Of Your Annual Performance Review]

Step 2: Find areas in which to excel. As part of your conversation, you should also determine a list of projects that could add extra value to the company that fall within the scope of your job.

It’s important to choose these projects in conjunction with your manager because you need to be sure that when you go above and beyond, it’s in areas that your company finds important. What’s more, you want your extra efforts to be recognized for what they are.

It’s helpful at this stage to come up with a way to document your performance. Remember Shelly—how she increased customer satisfaction by 10% and got 30% more referrals than average? These numbers make her value pretty undeniable, but they wouldn’t exist if she or her managers weren’t keeping track of them.

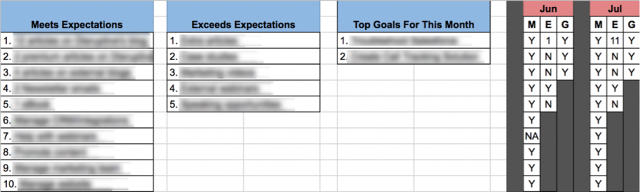

If you work in an area like sales, it’s pretty easy to document your performance with hard figures, but for many other jobs performance is less easy to quantify. Documentation is still important in these cases, but it may look a little different. For example, this is a scorecard my marketing director and I use to measure his performance each month (shared with his permission):

The first column contains a list of his basic job expectations. If he meets all of these he’s producing enough value to justify his base salary. The other two columns contain things that he can do to go above and beyond his normal duties to provide added value to the company.

This is a very simple documentation system, but it’s surprisingly effective. When it comes time for me to hand out bonuses and raises, I don’t have to wonder whether he’s earned it or not—I just look at the scorecard. If he’s consistently performing above expectations, then he’s adding extra value and he deserves to be rewarded.

Step 3: Make a plan and execute it. Finally, you need to put everything you’ve learned into action. If your goal is to increase your compensation at work, you can start by deciding how much more you would like to be making.

Take your current job expectations and salary as the baseline for what you’re worth to the company. Then realize that for every dollar that you hope to get in increased pay, you need to bring in three to five dollars to the business for your raise to make sense. Pick from your “above and beyond” list some projects that would add this kind of value to the company. Make a plan to complete these goals in addition to your regular tasks and present the plan to your manager.

Trust me, this will go over a lot better than the old, “I’m getting married so I need a raise” conversation. Your manager may not agree with every detail of your plan, but you will definitely come off as a motivated employee who really gets it. And even if your managers don’t buy in right away, it will be a great opportunity to discuss their priorities again and work together to come up with a plan that accomplishes things that really matter.

Don’t skip this important conversation. I’d hate to get a comment on this article saying, “I wasted six months doing what you said only to find out that nobody cared about my contribution.”

If you haven’t figured out by now, communication with your superiors is going to be a critical part of this whole process. Unfortunately, business plans are rarely static and you may have to chase a moving target, but if you’re willing to be flexible, you should be able to keep moving forward toward your goals.

Now, I know you’re probably thinking, “This all sounds great, Jacob, but it also sounds a little too idealistic. It would never work at my business.” Maybe not. I can’t predict every circumstance, and there’s a chance that yours is an exception. But isn’t it worth a try? The relationship between employee value and compensation holds just as true in “big ruthless corporations” as it does in more supportive ones.

For example, one of my employees recently related to me his experience at a prior company. This was one of those more stingy jobs and had a high turnover rate for entry-level employees. However, he applied the principles I’ve described. He developed a number of specialized skills and got deeply involved in some really important projects.

The miserly company was happy to be getting more out of him for the same pay—until the day he started looking at taking his skills elsewhere. His value was so great by then that the company would be set back months or years if he left, so when he suggested that he would need a 40% pay increase to stay, they felt like it was a worthwhile investment.

Despite the money-grubbing attitude of this company, he was providing so much value that he had become an asset they couldn’t afford to lose. As a result, he was able to negotiate a much better situation for himself. The moral of the story? If you feel that you deserve a raise, don’t get drunk and holler about it every Friday night. Take inventory of your worth, talk with your managers, and start working to become a more valuable asset.

https://www.firstsun.com/wp-content/uploads/2018/05/logo-min-300x123.jpg00First Sun Teamhttps://www.firstsun.com/wp-content/uploads/2018/05/logo-min-300x123.jpgFirst Sun Team2016-10-12 12:15:592020-09-30 20:50:30Your #Career : I’m A CEO—Here’s How I Decide Whether To Give You A Raise Or Lay You Off… This Exec Reveals the Arithmetic Companies Typically Use to Assess Employees’ Value.